#evergreen #research-piece #ai

Over the past two to three years, obscene amounts of capital have been poured into AI despite uneven, demonstrable ROI across industries. Yet valuations have reached eyebrow-raising heights. Which makes what happened in early 2025 all the more interesting.

Around February, a new term started spreading across news media and social feeds: the **SaaSpocalypse** - an over $1 trillion collapse in market capitalisation from the S&P 500 Software and Services index. This caught my attention, and I’ve chosen to deep dive into what actually happened.

First, we’ll examine what actually happened to the market and why indices matter. Second, we’ll investigate the real triggers - both the underlying structural factors and the specific catalyst events. Third, we’ll trace how three key players (Anthropic, OpenAI, and incumbent SaaS vendors) caused / responded to this shift and what their moves signal about the future. Finally, we’ll synthesise the evidence to answer the central question: is this truly an apocalypse, or a market correction with clear winners and losers?

## The Fall of S&P 500 Software & Services Index

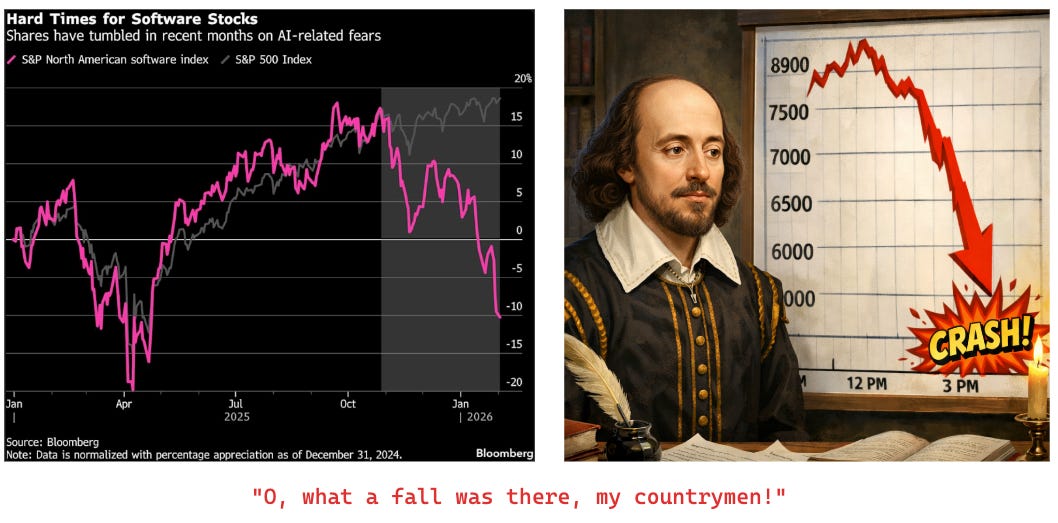

Since its peak in October 2025, the [S&P 500 Software & Services Index](https://finance.yahoo.com/quote/%5ESP500-451030/) has been undergoing a steady decline. To understand why that matters, it helps to first understand what an index actually is and how it works.

An [**index** is a curated list of company stocks](https://www.investopedia.com/terms/i/index.asp) grouped by something they have in common, in this case, companies operating in the software and services industry. Rather than tracking any single company, the index tracks all of them together, acting like a single thermometer for the health of the entire sector. When most of those companies are doing well, the index goes up. When confidence in the sector wavers, the index falls. It is a snapshot of collective market sentiment.

When an index drops sharply, the value of shares held by investors falls with it. If you bought a share for $100 three months ago and the index dropped 20%, that share is now worth around $80. Nobody wants to lose money, so investors start selling, trying to get out before things get worse. But that selling pressure pushes the price down further, say to $70. That is a 30% drop, which triggers even more selling. And so the spiral begins.

The only thing that stops this kind of spiral is **investor faith**. Investors collectively choosing to hold their positions rather than flee. Without that trust, each wave of selling feeds the next.

It is _worth noting that a falling index_ **_does not always mean_** _investors have lost faith in those specific companies alone_. Broader forces like rising interest rates, macroeconomic uncertainty, or money rotating into other sectors can all drag an index down. But when the drop is as sharp and sustained as this one, it most visibly signals eroding confidence in the sector as a whole, albeit temporarily.

By mid February 2026, about [2 trillion dollars of market cap had been erased from the S&P 500 Software & Services Index since its October 2025 peak](https://www.techbuzz.ai/articles/the-2-trillion-saa-spocalypse-how-to-become-unsloppable-in-2026). And half of this vanished in the first 2 weeks of late Jan / early Feb 2026. It was around this time, an equity trader Jeffrey Favuzza at Jeffries coined the term [“Saaspocalpyse” - a dramatic downturn for software-as-a-service stocks. “The prevailing mood is to sell at any cost,” he noted.](https://www.bitget.com/news/detail/12560605181026) And since there was a "fancy term” to this phenomenon, the internet picked it up and went berserk.

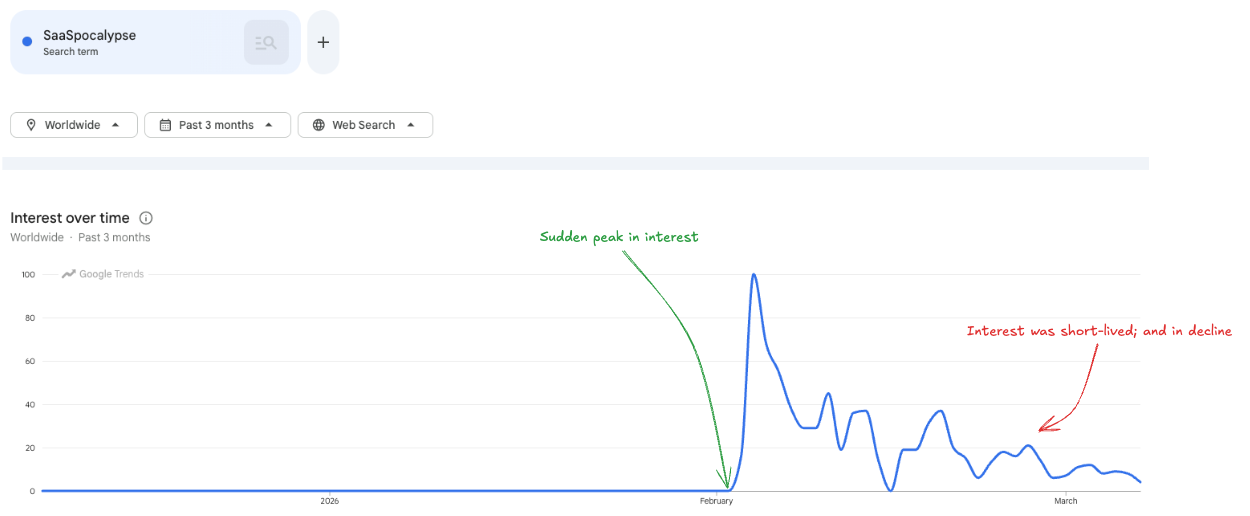

Google Trends (Annotated by the author)

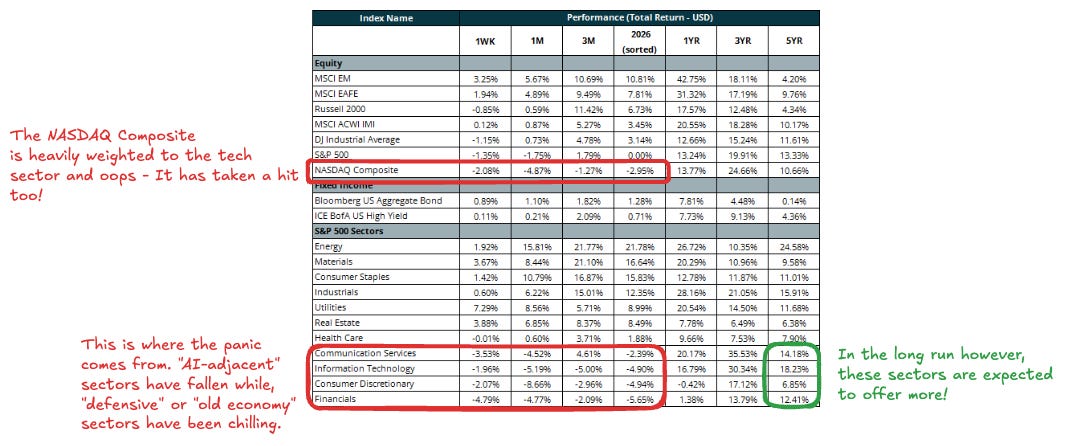

The below [market commentary from Sequoia](https://www.sequoia-financial.com/insights/ai-disruption-fears-spread-to-multiple-industries/) (Feb 17, 2026) offers a bit more nuance on this collapse. Of all the sectors in the S&P 500, it is the “AI-adjacent” sectors that have in fact taken a beating, whil “defensive” or “old economy” sectors have shown growth. This underscores the idea that there is something happening specifically to software. However, what most articles around the Saaspocalpyse miss out on is the green rectangle below. In the longer 3-5 year period, the index values are expected to recover and grow strongly. Of course, this is a very distant future that could look totally different when it arrives[1](#footnote-1). But, it goes on to show that it is definitely not all gloom and doom.

Annotated by the author

## What triggered the sell-off?

A surprising number of financial news articles talked about how this collapse was triggered by an “in-house legal tool” released by Anthropic. As far as I can tell, there was no such magical tool. What actually happened was that Anthropic released 11 plugins for Claude Cowork, including a legal plugin, on January 30, 2026. _A plugin for a product still in preview triggered a panic sell-off. Do I cry or do I laugh?_

As per Google trends, “Saaspocalypse” was strongly linked to “Anthropic”.

But the index had already been falling since October 2025, a full three months before those plugins existed. So, while this “doom” label was new; the decline was already on.

So what was actually driving the drop from October 2025 onward, before Anthropic released those plugins? As per [S&P Global](https://www.spglobal.com/market-intelligence/en/news-insights/articles/2026/2/software-sell-off-may-be-overdone-yet-exposes-deeper-concerns-97965687), a few things -

1. SaaS growth rates had already been declining since the pandemic-era boom of 2021-22 and had basically plateaued by early 2025. October was simply when the **market decided it had been too generous with valuations on companies no longer growing fast**.

2. At the same time, **IT budgets had quietly started shifting toward AI infrastructure**, with CFOs saying “pause new seats, explore AI” as early as mid-2025.

3. **Corporate layoffs were also directly hurting per-seat SaaS revenue**, since you literally lose seats when you cut headcount. While related to AI, this has nothing to do with AI killing SaaS because its better. It’s just the exposure of a traditional business model that is easily affected by AI-related layoffs.

4. Finally, **high-multiple software stocks were vulnerable the moment growth expectations flatlined**, and by October enough earnings reports had come in below expectations that institutional investors started rotating out.

Another obvious reason of this decline is the market looking at AI as _subtractive_. AI will lead to reduce in SaaS costs, AI will lead to reduced headcount, AI will lead to reduced barrier to build apps - the infamous “vibe coding” rhetoric. Take for example the case of Gartner - Its value tanked from a March 2025 peak to a severe low in August 2025, and continued to drop to another severe low in March 2026. This is because of the investor assumption that [new AI tools are making enterprise-level subscriptions to Gartner’s services obsolete](https://www.fool.com/investing/2025/09/02/these-were-the-sp-500-indexs-worst-performing-stoc/).

Source: https://www.fool.com/investing/2025/09/02/these-were-the-sp-500-indexs-worst-performing-stoc/

**How does Gartner respond?** - It rolls out its own [AI application, AskGartner](https://www.gartner.com/en/products/ask-gartner) on top of its proprietary data to ensure it offers way more value than a generic AI tool.

But, in a nutshell what this section tells me is that the Anthropic plugin launch just sped up something that was already happening.

## How did Anthropic contribute to the panic?

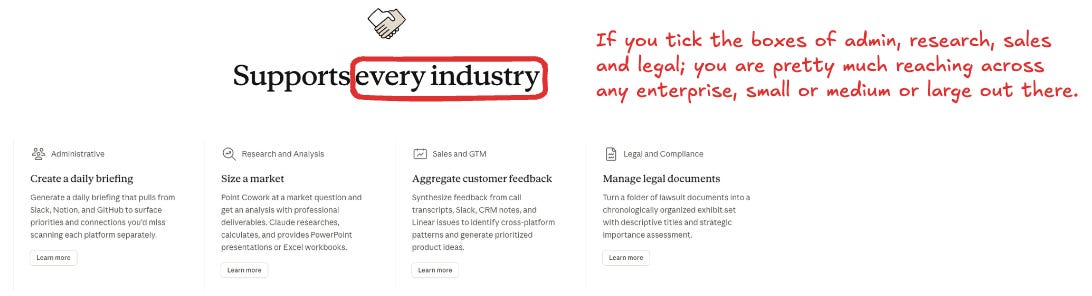

On January 30, 2026, Anthropic released an [open-source set of 11 plugins for Claude Cowork, covering functions like sales, finance, legal, HR, marketing, data, and more](https://github.com/anthropics/knowledge-work-plugins). Each plugin bundles tools, connectors, and slash commands so Claude can plug directly into the software stack a team already uses.

To understand why this [spooked investors](https://www.reuters.com/business/media-telecom/ai-concerns-pummel-european-software-stocks-2026-02-03/), it helps to understand what [Cowork](https://claude.com/product/cowork) actually is. Think of it as having a coworker who sits on your system: you describe the outcome, step away, and come back to finished work. It reads files, edits documents, runs multi-step tasks, and coordinates sub-agents to work in parallel. When you layer specialised plugins on top of that - legal contract review, financial reconciliation, sales outreach - you essentially give a company a ready-made reason to pause hiring in those functions.

Source: https://claude.com/product/cowork

Combined with IT budgets already shifting toward AI infrastructure, Cowork made the “replace seats with agents” thesis feel very concrete, very fast.

The bigger picture here is summed up well by Marco Kotrotsos - [Cowork is evidence that not just developers, but all knowledge workers will eventually shift from being “doers” to being “architects and designers.”](https://kotrotsos.medium.com/claude-cowork-is-a-game-changer-ec4037ef0ba4) The agents become the doers. Whether you believe that fully or not, you can see why it rattled the software sector.

But Cowork is no silver bullet. Two issues stand out. The first is **prompt injection** - where attackers embed hidden instructions in content to hijack agent actions. This is described in the [OWASP LLM Top 10](https://genai.owasp.org/llmrisk/llm01-prompt-injection/), appearing in 73% of production deployments. OpenAI acknowledges it "may never be fully solved." Anthropic has implemented a three-layer defense (model reinforcement, content classifiers, permission controls), achieving 1% injection rates in Claude Opus 4.5. This remains a 2027-2028 concern before reaching enterprise comfort levels.

The second is **token consumption**. Multi-step workflows easily consume 5-10 million tokens monthly, with real enterprises seeing costs spike from $1,200 to $4,800 (a 300% increase). However, solutions are already deployed at scale: [prompt caching](https://www.anthropic.com/news/prompt-caching) saves 90% on reused content (Anthropic) and 75-90% (OpenAI). Combined optimizations (token budgeting, tiered models, batching) reach 60-80% cost reductions.

## How did OpenAI contribute?

### The Release of OpenAI Frontier

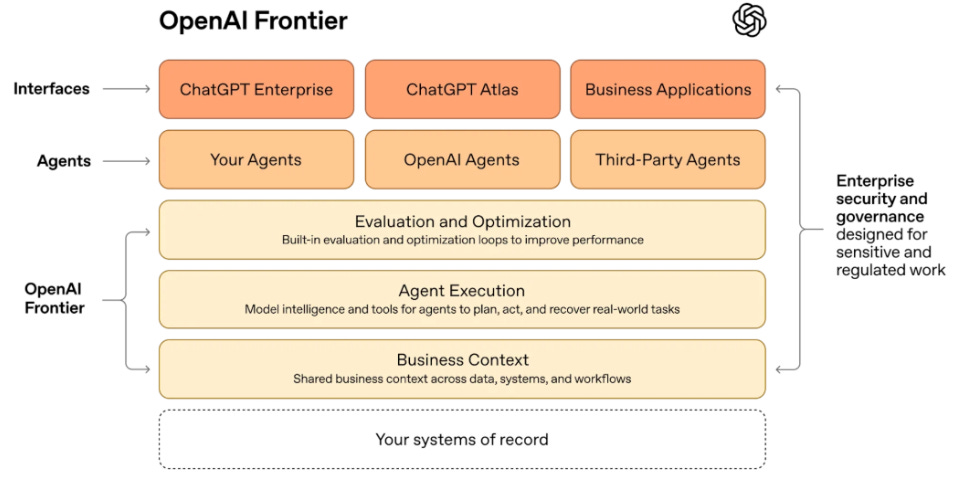

On February 5, 2026, OpenAI introduced [Frontier](https://openai.com/business/frontier/), an enterprise platform designed to help large companies build, deploy, and manage AI agents at scale. The pitch is simple - treat AI agents like employees. Each agent gets onboarding, shared business context, explicit permissions, and a feedback loop to improve over time, the same things a company would give a new hire.

Source: https://openai.com/business/frontier/

The diagram above essentially says - OpenAI sits at the centre of your enterprise, your systems of record plug into it, and your SaaS tools become optional. The agents handle the work. Your SaaS subscriptions do not need to. They can just be “plugged in” to the OpenAI core.

Because Frontier is built on open standards, it works with agents built inside or outside of OpenAI, including those from Google, Microsoft, and Anthropic. That sounds generous, but it also means OpenAI is positioning itself as the layer that sits above everything else.

Source: https://openai.com/business/frontier/

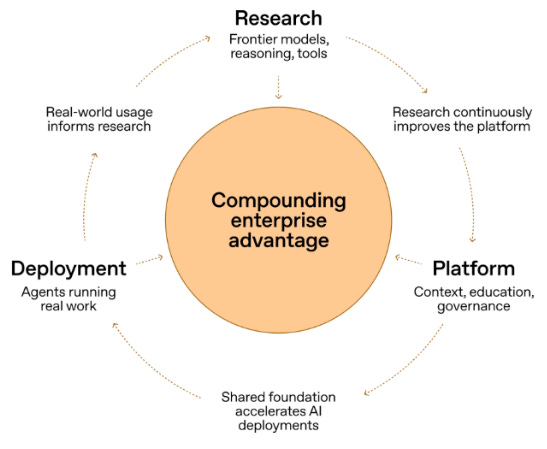

The “compounding enterprise advantage” diagram in their materials makes this explicit - real-world usage informs research, research improves the platform, the platform drives more deployment, and so on. What that loop quietly means is that the more you use it, the more locked in you become. _Say hi to vendor lock in as a service._

### The Hiring of Peter Steinberger of OpenClaw

OpenAI also hired Peter Steinberger, the creator of OpenClaw, to [drive the next generation of “personal agents”. OpenClaw will continue as an open-source project under a foundation that OpenAI will support.](https://techcrunch.com/2026/02/15/openclaw-creator-peter-steinberger-joins-openai/) OpenClaw, which had previously gone through a couple of name changes, had gone viral for being a genuinely usable personal agent that ran on your own hardware and connected to messaging apps and calendars. While it was a security nightmare on more occasions than one, it still took the world by storm. It did to agents what ChatGPT did to generative AI - overnight democratisation.

Steinberger’s goal as stated on his [blog](https://steipete.me/posts/2026/openclaw) is to “build an agent that even my mum can use”. That is not to be read as a casual line. It is in every way aligned with OpenAI’s vision to make it easy to build and deploy agents.

**Why does any of this matter for the SaaSpocalypse?** Because it signals where enterprise spending is going. Businesses are increasingly thinking about building agents to get things done, rather than buying a pre-packaged app for every function. That is a fundamental shift in how software gets purchased.

## How did SaaS respond? Featuring Salesforce.

During its Q4 FY26 earnings call on February 25, 2026, [Marc Benioff made it very clear that he is not worried about the SaaSpocalypse](https://techcrunch.com/2026/02/25/salesforce-ceo-marc-benioff-this-isnt-our-first-saaspocalypse/). He mentioned the term at least six times, saying _“You’ve heard about the SaaSpocalypse? And it isn’t our first. We’ve had a few of them,”_ referencing the 2008 financial crisis, the 2016 slowdown, and the Covid pandemic as prior moments when SaaS was supposedly finished.

His central argument is that _agents do not replace SaaS, they need SaaS to deliver value. You still need the data, the systems of record, the context. Agents just sit on top of it_.

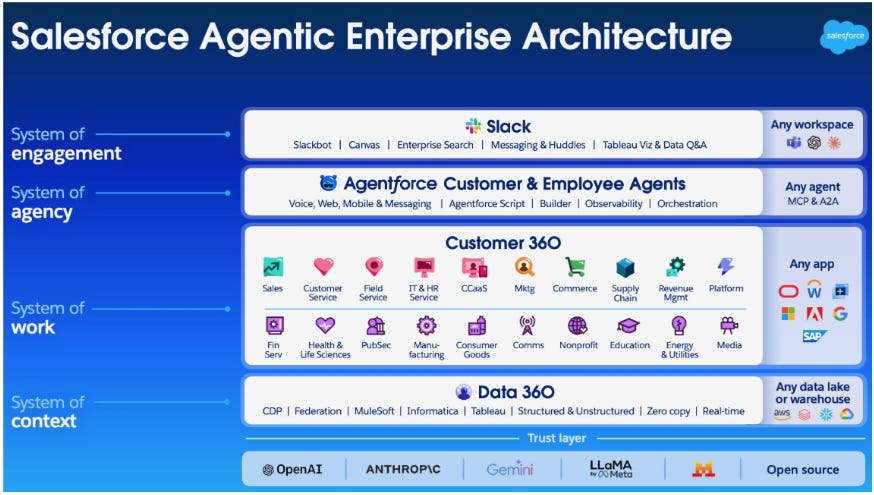

Salesforce reported [FY26 revenue of $41.5 billion, up 10% year-over-year, with Q4 revenue of $11.2 billion, up 12%](https://www.salesforceben.com/huge-agentforce-growth-in-salesforce-q4-as-benioff-mocks-saaspocalypse-narratives/). The company is also becoming what it calls an “Agentic enterprise” itself, pointing to its Agentforce platform as evidence that existing SaaS can adapt rather than collapse. For example, take a look at the Salesforce Agentic Enterprise Architecture here.

I find it hard to believe that this diagram has any other purpose but to clap back at Open for their Frontier architecture - To send a passive-aggressive message back to OpenAI’s Frontier architecture - _You, OpenAI are just another party that will integrate INTO US. SaaS is big, Salesforce is bigger and LLMs are valuable only with proprietary data that rests within incumbent SaaS companies_. One almost needs to squint to see the OpenAI, Anthropic logos on this diagram.

The honest question, though, is how many smaller SaaS companies can afford to make this pivot into being Agentic. Salesforce has the scale, the data layer, and the brand to reframe itself as an Agentic platform. Most mid-sized and small SaaS vendors do not.

### The Agentic Work Unit and Outcome-based pricing

Salesforce introduced a new metric called the [Agentic Work Unit](https://www.salesforce.com/news/stories/agentic-work-units/), or AWU. One AWU is one discrete task completed by an agent: a prompt processed, a reasoning chain completed, or a tool invoked. It is arguably the [first serious attempt by a major software vendor to define what might replace the per-seat model](https://businessengineer.ai/p/the-agentic-work-unit). Salesforce reported 2.4 billion AWUs delivered to date across Agentforce and Slack, growing 57% quarter-over-quarter, and over 19 trillion tokens processed to date.

Whilst [Thomas Wieberneit raises an excellent point on why the AWU is a vanity metric due to its big assumption that “doing work” = “achieving outcomes”](https://aheadcrm.medium.com/the-illusion-of-value-why-salesforces-agentic-work-unit-is-the-new-bad-query-of-the-ai-era-b8dffb6d3de0); the AWU is still a great first step in the right direction as it looks to use a “better” metric for usage-based pricing.

However, [outcome-based pricing is pretty much where agents should look to go towards in order to maximise value for the paying customer](https://customerthink.com/which-ai-pricing-models-work-best-for-customers/). Currently, most pricing of AI is usage-based (similar to SaaS) i.e tokens consumed. However, with usage-based pricing, the onus of “being efficient” is on the consumer. If a consumer does not use LLMs efficiently, then they literally pay a hefty price.

However, with outcome-based pricing, if an agent does not achieve an expected outcome, the vendor absorbs the costs and not the customer. This implies greater “skin in the game” for the vendor.

## So, is there a SaaSpocalypse?

The narrative has cooled. Google Trends show declining interest, valuations have stabilised, and the panic that gripped the market in February 2026 has subsided. But the structural questions remain.

**The Real Winners and Losers**

The ones who will genuinely struggle are not the big incumbents. They are the smaller SaaS vendors and thin-wrapper AI companies launched over the past two to three years. This is specifically because they do not have deeply entrenched systems with enterprises and thus have no "real" advantage.

The winning categories are somewhat clear - **Vertical SaaS companies** serving healthcare, agriculture, construction, or finance are thriving. [Growing 400% year-over-year](https://qubit.capital/blog/rise-vertical-saas-sector-specific-opportunities), they build defensible positions around context depth (the "context graph"), domain-specific data, regulatory compliance, and user-generated network effects - not feature parity. Meanwhile, small and medium-sized businesses (SMBs) now access enterprise tools through AI-driven self-service, [expanding the addressable market 10x downward](https://www.weforum.org/stories/2026/01/ai-mid-market-business-growth/). Small vendors that niche down have real paths forward.

**The Incumbent Advantage - But With Conditions**

Incumbents like Salesforce and Gartner have the scale, data, and customer trust to pull off the pivot to agentic enterprises. [Salesforce’s Agentforce reached $500M+ ARR with 330% growth in 2025](https://www.salesforce.com/news/stories/2025-recap/), reaching 12,000 customers. As far as its AI-native challengers are concerned, Anthropic’s Cowork remains in research preview and OpenAI’s Frontier is only weeks old. The LLM providers are not the center of the enterprise stack; SaaS vendors are, and they control access.

But incumbents face a pivotal challenge: the **per-seat pricing model is obsolete**. HubSpot transitioned to credit-based consumption and grew 20%. [Zendesk charges $1.50-$2.00 per AI-resolved ticket](https://www.eesel.ai/blog/zendesk-ai-pricing-complete-breakdown-by-plan-2025); [Intercom’s Fin AI charges $0.99 per resolution with 393% growth](https://www.chargebee.com/blog/pricing-ai-agents-playbook/). Hybrid models dominate: [61% of SaaS companies now blend per-user, usage, and flat-rate pricing](https://www.flexera.com/blog/saas-management/from-seats-to-consumption-why-saas-pricing-has-entered-its-hybrid-era/). Industry analysts predict outcome-based pricing will grow significantly, with adoption already visible among early movers.

**The Execution Speed Paradox**

AI companies ship weekly/monthly while SaaS incumbents ship quarterly. Yet faster shipping hasn’t translated to market capture. [Gartner predicts 40% of agentic AI projects will be canceled by 2027](https://www.gartner.com/en/newsroom/press-releases/2025-06-25-gartner-predicts-over-40-percent-of-agentic-ai-projects-will-be-canceled-by-end-of-2027) - not from missing features but governance gaps, data architecture challenges, and talent scarcity. The gap between pilot capability and production readiness remains the real constraint.

Legacy system integration, data readiness, and compliance block the majority of AI project failures. Incumbents’ advantages - proprietary data, workflow control, enterprise trust, and integration depth - matter more than velocity once production readiness becomes the constraint.

**The Verdict**

[It is not an extinction-level event. It is a cleansing fire](https://subramanya.ai/2026/02/23/the-saaspocalypse-a-survival-guide). The market reprices the assumption that SaaS seats are worth their historical valuations in an age when agents can perform work once done by multiple humans. Valuations contract. Consolidation accelerates. Viable niche players carve defensible positions. The market finds a new floor.

But that correction is real, and the path through it remains uncertain for the vast middle of SaaS companies caught between being big enough to invest in transformation and too small to survive the CapEx required to build world-class Agentic platforms.

[1](#footnote-anchor-1) The core assumption here is that AI disruption _complements_ software companies rather than _replacing_ them.